SBTi’s net zero blind spot: Carbon removal can’t wait

SBTi’s cautious stance on carbon removal won’t get us to net zero.

The Supercritical newsletter bringing you sharp analysis, market intelligence, and practical strategy to keep you ahead of the carbon crunch. No fluff. No filler. Just what you need to know to lead on carbon removal.

This month’s edition comes from Mai Bui, Supercritical’s Director of Climate Science, and a newly appointed member of the Science Based Targets initiative (SBTi) Expert Working Group (EWG) on Carbon Dioxide Removal (CDR) in recognition of her independent expertise. The views expressed here are her own.

SBTi plays an outsized role in shaping corporate climate action. As the most widely adopted framework for setting corporate net-zero targets, it is one of the biggest influences on CDR demand, effectively dictating who buys CDR and when. That’s why the latest draft of the Corporate Net Zero Standard (V2.0) deserves serious scrutiny.

While V2.0 takes steps forward, many in the CDR community expected more. The proposed guidance fails to deliver the ambition needed to scale carbon removal. By sidelining Scope 3 emissions and framing CDR as a last resort, the guidance risks holding the market back at precisely the moment it needs to accelerate.

The elephant in the room: SBTi is sidelining Scope 3, and CDR with it

The new draft of SBTi’s Corporate Net Zero Standard (v2.0) makes progress in some areas, but it falls critically short where it matters most: scaling carbon removal. A key positive development is a proposed requirement to set near- and long-term targets for CDR alongside interim targets. The separation of Scope 1, 2 and 3 targets and additional detail are also welcome changes. But that’s where the ambition stops.

SBTi’s updated framework explicitly excludes the use of carbon removal credits for Scope 2 and 3 emissions. Companies are only expected to neutralize Scope 1 residual emissions in the lead up to their target net-zero year. For companies that are not expected to have residual emissions, SBTi is exploring whether limited use of removals may be permitted for justified hard-to-abate emissions. No guidance is offered for addressing gross emissions in the decades leading up to the net-zero year. These emissions are significant and companies choosing to address these should receive recognition.

That’s a major problem.

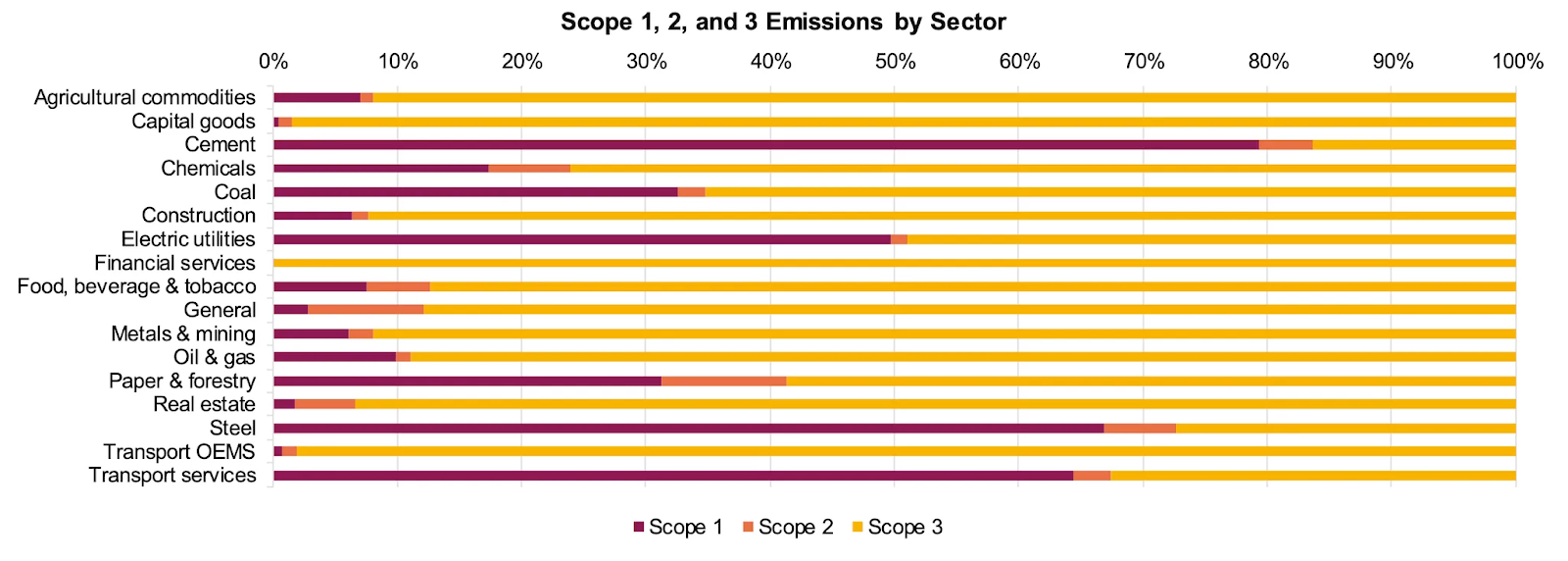

Scope 3 emissions typically account for the majority of a company’s footprint. This is where carbon removal is likely needed most. Although SBTi’s draft offers guidance on how to set Scope 3 targets - either supplier engagement or mitigation - there is no clear route to address them. This is because Scope 3 emissions are outside a company’s direct control, meaning they’re also the hardest to influence and reduce.

Without Scope 3 coverage:

Demand for CDR will remain artificially low and CDR will struggle to scale.

Companies will focus narrowly on Scope 1 emissions while their largest climate impacts from Scope 3 emissions remain unaddressed.

The same logic applies to how SBTi is proposing companies approach CDR durability. While the “like-for-like” option may appear rigorous, it’s not a viable path toward market scaling. With less upfront removal required compared to the “gradual transition” approach, companies will take the cheapest—and least impactful—route available. SBTi’s job isn’t to build and scale the CDR market, but it does have an enormous influence on how it evolves. If they continue to provide guidance in isolation from market conditions, demand will stall, supply won’t scale, and CDR with 1000+ years permanence will not exist when we need it most.

Take the steel, cement, oil or gas industry—sectors with significant Scope 1 emissions, and notably lacking in SBTi targets. It’s unrealistic to expect voluntary reductions or removals from these companies; they will not decarbonize unless market pressures force their hand. If SBTi required companies to neutralize Scope 3 emissions, downstream customers would drive that pressure, leaving upstream emitters like oil and gas with a choice: either cut emissions and invest in CDR, or lose business to lower-carbon competitors.

Source of figure: CDP report

SBTi needs to rethink its approach to carbon removal. If the goal is credible net zero, the framework must enable companies to use CDR to neutralize Scope 3 emissions. Even if companies set supplier engagement and mitigation targets, Scope 3 emission activities are still outside direct control and most companies have limited influence on suppliers’ emissions. SBTi must champion the pathways that can feasibly align with 1.5℃ IPCC targets and provide a viable route to real impact.

In the absence of ambitious guidance, it’s up to companies to lead. The science is clear: you need carbon removal. Delaying action because the current versions of guidance don’t require it is a fast track to failure.

Playing it safe won’t scale carbon removal

When it comes to CDR, SBTi’s proposed guidance is missing the mark. It treats carbon removal as something to be minimized rather than mobilized. Science tells us that we don’t have the luxury of viewing CDR as a future problem. Reaching net zero requires aggressive scaling of carbon removal today.

Instead of framing CDR as a last resort, with rhetoric around guardrails rather than pathways, we must consider the market realities we’re up against:

CDR supply won’t magically exist in 2049 when companies finally decide they need it.

The technologies and projects we’ll rely on in the years leading up to 2050 require financing and strong demand signals today to scale.

Without early investment (through mechanisms like offtakes) the market won’t develop at the pace required.

Reduction and removal must happen in parallel. If CDR is sidelined while every reduction option is exhausted, the carbon removal capacity needed to meet net zero won’t exist when it’s time to address residual emissions. Scaling CDR takes decades. If we don’t start now, it won’t be there when we need it.

What’s in the draft

SBTi’s Corporate Net Zero Standard V2.0 brings several structural updates. Here’s a quick guide to what’s in SBTi’s draft CNZS v2.0 and areas where SBTi is seeking feedback:

Scope 1 and 2: More defined criteria

Separate targets now required.

Aligned with the Sixth Assessment Report (AR6) from the International Panel on Climate Change (IPCC) and the latest Net Zero Emissions by 2050 Scenario (NZE) from the International Energy Agency (IEA).

Scope 2 split into:

Location-based targets.

Market-based OR zero-carbon electricity.

Clearer rules on Energy Attribute Certificates (like renewable energy certificates).

Scope 3: Major updates to approach

Refined target boundaries based on emissions relevance.

Drill down into all Scope 3 emissions categories, identifying the most significant and emission-intensive.

Greater emphasis on supplier alignment and indirect mitigation.

Companies will need to set either (i) supplier engagement targets, or (ii) mitigation targets for all significant categories of Scope 3 emissions.

Feedback sought on thresholds, feasibility, and traceability.

CDR: Limited application and unlikely to help it scale

CDR limited to neutralizing residual emissions (defined as unaddressed Scope 1 emissions after the company has done all they can to abate/reduce) near net-zero target year.

Companies will need to set interim targets for carbon removal (e.g., targets for 2030, 2035, 2040 etc.)

Companies have three options for how they address their residual emissions

Option 1: Mandatory carbon removal target (larger category A companies)

Option 2: Recognized for setting optional carbon removal targets (small category B companies)

Option 3: Increased Scope 1 abatement (reduces total removal required) and setting interim carbon removal targets

New minimum permanence requirements are yet to be decided.

Companies must choose between two permanence approaches:

Like-for-like: CDR permanence is matched to atmospheric lifetime of greenhouse gases (GHGs) such as methane. This approach will require less upfront removal, but residual emissions of most buyers are mainly CO2 (atmospheric lifetime of 1000 years) so most buyers will need to procure 1000+ year minimum permanence. Those with methane emissions (12-year lifetime) can purchase low permanence CDR of at least 12 years (e.g., NBS removals).

Gradual transition: Companies increase share of high permanence (1000+ years) removal over time. Whilst the total cumulative removal is the same, this approach will require more removal to be purchased initially, with the option of using a higher share of conventional CDR options with 100+ year permanence (includes biochar and potentially very high quality NBS). At each interim target, the share of high permanence CDR (1000+ years) will increase.

At Supercritical, we believe the gradual transition approach is not only more cost-effective for buyers, but also the only viable path to scale. By allowing companies to start with a higher share of conventional CDR upfront and phase in more durable options over time, gradual transition sends an immediate demand signal to the market. That’s how carbon removal supply grows: through early, bankable offtakes.

Beyond Value Chain Mitigation (BVCM): Recognized for efforts

Recognition for actions like carbon credits, direct financing of mitigation projects or conservation of ecosystems.

CDR and BVCM: Unclear if purchase of CDR credits qualifies, but financing projects likely to receive recognition.

Validation cycle: More accountability & shift towards high-quality data

Regular progress checks, alignment metrics, and a push for higher data quality.

Clearer guidance on how progress towards targets is assessed and validated.

Company categorisation system

New categorization system based on company size, emissions, and geography.

Companies need to determine the applicability of SBTi sector-specific requirements.

How will these changes impact the market?

The above updates introduce clearer categorization for companies, sharper requirements for Scope 1 and 2 emissions, and improved data assurance mechanisms.

The new company categorization system provides a clear structure for companies to follow, with companies allocated into either Category A or Category B.

Category A (larger companies) must address Scopes 1, 2, and 3.

Category B (smaller companies) are only required to address Scopes 1 and 2.

The graphic below shows which thresholds are considered for categorization (emissions, balance sheet, net turnover worldwide, employee number, geographical consideration).

The draft proposal sets out what is required of Category A and Category B companies, eliminating much of the guesswork around what companies do (and do not) need to do. This is a welcome step forward from the SBTi.

Smart buyers aren’t waiting for perfect guidance

We recognise that SBTi faces a near-impossible task: developing a standard that’s scientifically rigorous, politically viable, and practical for thousands of companies. But climate science, and market reality, can’t wait for perfect consensus.

There is a silver lining: catalytic buyers, the ones who will shape the carbon removal market for decades to come, aren’t waiting for SBTi’s permission. Google, Microsoft, and other leaders are already locking in long-term CDR agreements because they understand two things:

CDR is a parallel priority, not a postscript. Reduction and removal must happen together.

The market will reward early movers. Delaying means facing higher prices, tighter supply, and credibility risks when net-zero deadlines loom. Or worse, missing targets entirely.

Any company serious about net zero, no matter its size, is putting budget into carbon removal. The smartest ones are choosing offtakes. At Supercritical, we work with buyers who recognize that it’s ambition, not compliance, that will define credible climate action over the next decade. That means:

Locking in permanent CDR supply now through well-structured offtakes.

Diversifying portfolios across methods that meet both climate and business needs, whilst also minimising risk.

Thinking ahead of the market, not reacting to it.

Waiting for others to get it right isn’t a strategy. Acting decisively and in line with the science is. Get in touch today to speak with one of our experts about your procurement strategy.

What’s new at Supercritical?

📅 Upcoming event: Supercritical hosts the CDR Leadership Forum

We're bringing together the leaders shaping the future of carbon removal for an evening of conversations, bold ideas, and rooftop networking, part of London Climate Action Week. Hear from CDR experts at Google, Exomad Green, Puro.earth, Capgemini and Charm Industrial.

Save the date: June 25.

Register here

🎤 On stage: Michelle You at Carbon Unbound NYC

Supercritical is heading to Carbon Unbound East Coast. Our CEO Michelle You will be speaking on scaling permanent carbon removal, alongside other industry leaders. Meet our team on the ground: we'll be in New York connecting with buyers, suppliers, and innovators who are building the future.

▶️ Webinar: Mastering CDR Procurement

Live: Thursday 8th May, 4pm BST | 11am EST

Carbon removal procurement is getting more complex and more urgent. Our next webinar breaks down the strategies that smart buyers are using to build permanent, cost-effective portfolios.

Register here

🧠 Latest articles and coverage

World Economic Forum: The urgent need to scale carbon removal

Why companies must move beyond avoidance and why CDR needs to scale now.

The carbon removal procurement journey: How to buy high-quality credits for your Net Zero goals

A practical guide for navigating a fragmented and fast-moving market.

Ecovadis invests in Supercritical credits: Read the full story

Another leading company locking in high-quality biochar credits.

🛠 Product update: New features in Credit Manager

Portfolio management just got a major upgrade. Our Credit Manager tool give you clearer visibility and more control over your CDR strategy.

Access it in our marketplace

🌱 Exomad Green offtakes

We’ve extended our Supercritical x Exomad Green partnership, giving you access to one of the most bankable biochar offtake options on the market.

Lock in supply while capacity lasts.